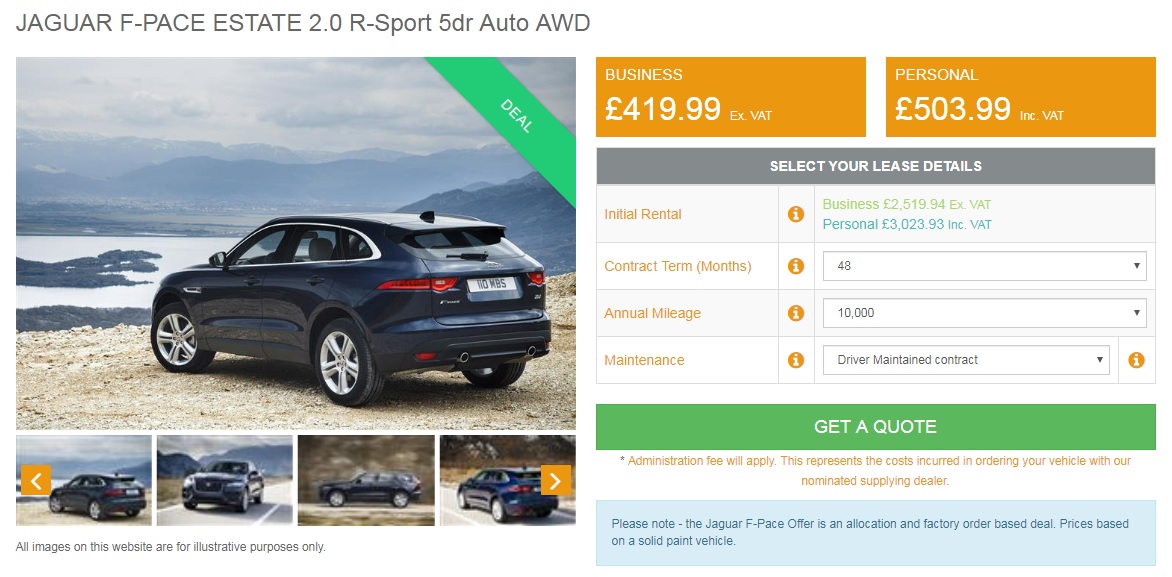

Thank you to our existing personal leasing customer, from Crawley (West Sussex), for sending through pictures of their new replacement lease car – the Jaguar F-Pace SUV.

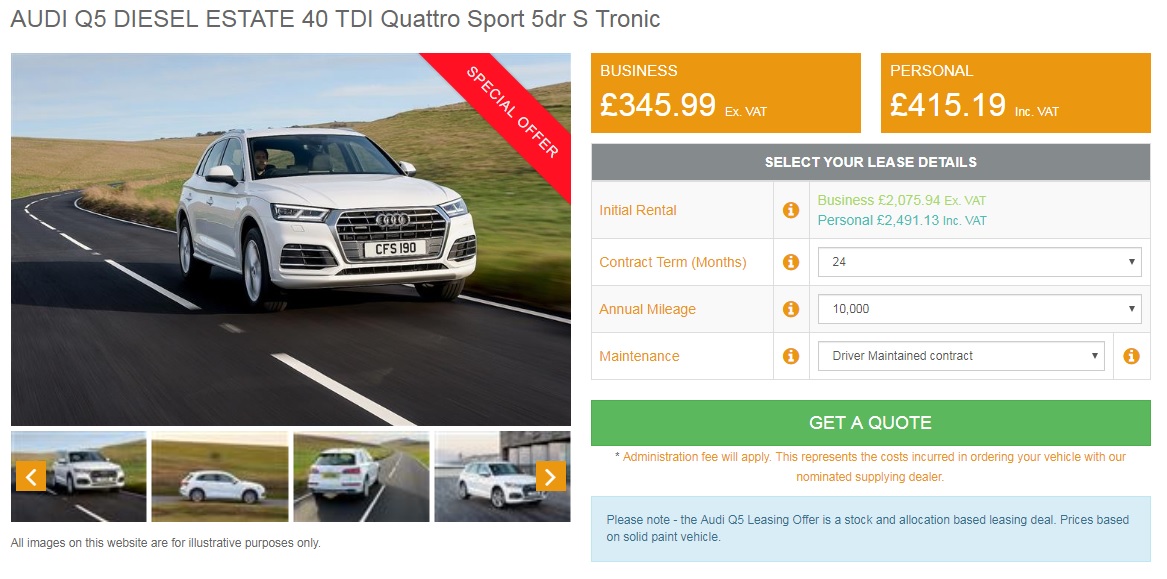

Our customer was actually replacing a current Personal Contract Purchase (PCP) agreement with us on their Audi Q5 and instead going the contract hire route.

So is a personal contract hire agreement just better than a PCP? There is not a simple yes or no answer to this question; while traditionally a PCP has been the foremost route for individuals to procure a new car, contract hire has grown considerably as a new way for customers to consider operating a vehicle.

Take our customer here for example, their initial contract was a four year PCP agreement on the Audi, with a view that they might purchase the vehicle at the term. With a PCP, you have a Guaranteed Future Value (GFV), which is a pre-set amount at the outset of the contract and is based on the car you are buying, the term you need (2 – 5 years) and your annual mileage (5,000 – 50,000 per annum).

The GFV, or balloon as it is sometimes referred to, is there to show the customer what they need to pay in full to own the car at contract cessation (some finance companies will charge a purchase or option fee along with this).

In our example, as we got closer to the end of the contract the customer became more interested in new and exciting product developments across the Audi Q5, Mercedes GLC and Jaguar F-Pace range.

Like many PCP customers, the allure of keeping the vehicle for longer than the four year term soon dissipated. Their existing vehicle would be well outside of its warranty, the technology fell well short of the modern innovations and there was a concern that more major servicing bills would start to appear.

So in the example above, we had a very common result, whereby the customer goes ahead with the PCP with the view they will keep the car for a longer period of time or they will have “equity” at the end of the contract.

While some customers do experience some of these benefits, the stark reality is that many customers do not and they need to be more savvy about their approach to car ownership (or usership).

The first, and most important rule, is that a car is not about “making money”.

All modern vehicles depreciate and will cost the customer; the aim is to minimise this cost and process this via an agreement which best meets your needs and requirements.

So where does a PCP start going wrong? The traditional payment-led model, whereby a customer goes into a dealership and says I want to spend £x per month on a new car, can cause come issues. While the broker or dealer can often achieve the monthly budget, the way in which they do it does not always meet the customer’s needs. For example if a customer needs 15,000 miles and a 3 year agreement but their budget affords then a 4 year term and 10,000 mile contract, if they sign up for the latter just to satisfy a budget, they are effectively creating issues at a later date.

This is where some of the “negative equity” can creep into it, as a customer will have a vehicle which is over-mileage and will not realistically meet its GFV/Balloon.

But surely you can just hand the vehicle with a PCP? Again, there are various misnomers on how the product works exactly. With a PCP, you can ask for an early termination in exactly the same way as a contract hire agreement. The finance company will then present the option to a) pay an amount to own the vehicle; or b) pay an amount to them for it to be collected. If a vehicle is collected, this will still be inspected for condition and mileage in exactly the same way as the contract hire agreement. If your vehicle is over-mileage, you will get an excess mileage bill. For customers who have paid over half of the total amount payable (including the initial payment, monthly payment and the GFV) you may be able to voluntary terminate the vehicle. However, this notion of just handing back your car without a penalty needs to be accepted as false; it just doesn’t work in that way. I

f you do voluntarily terminate and the car is over-mileage or in a poor condition, your will be charged. It is that simple.

So a PCP is something a customer should be alarmed about? Absolutely not. A PCP is still a valid and genuine finance product for a new car. However, payment-led approaches and the cavalier dealership saying “it will be ok in 3 years” or “just come and see me when you want to swap it” is a thing of the past. The Financial Conduct Authority (FCA) have made this clear to all brokers and dealerships. When you get the new car, consider how each finance product works and also ensure this meets your needs and requirements. If a proposition is not affordable, you should not go ahead with this.

In terms of the car shown here, the Jaguar F-PACE DIESEL ESTATE 2.0d R-Sport 5door Auto AWD, this is based on the following configuration:

· Santorini Black Metallic Paint

· Perforated grained leather – Ebony/Light Oyster with Contrast stitching

· Etched aluminium veneer

· Morzine headlining – Ebony

· 19″ 5 split spoke grey diamond turned finish alloy wheels – style 5038

As standard the car includes power tailgate/boot lid, 19” alloys, rear view camera, xenon headlights, 80W sound system, body coloured externals, load space scuff plates, 8-way manual adjustable front seats, climate control, xenon headlights, navigation with a 10” screen, ambient interior lighting, sport seats, cruise control, emergency brake assist, 360 degree parking aid, electric heated door mirrors, front and rear parking aid, heated fronts seats, green tinted heat insulating glass, rain sensing wipers, ASPC, AEB and forward facing camera, hill launch assist, hill start assist, traction control, premium carpet mats, android auto/ Apple carplay, lane departure warning system, lane keep assist, auto dimming rear view mirror, Bluetooth, DAB radio, InControl protect, dual tailpipes, adaptive cruise control, approach illumination, automatic headlights, fog lights, headlight power wash, LED tail lights, leather steering wheel, multifunction steering wheel, connect pro pack, trailer stability assist, keyless start, perimeter alarm and immobiliser. In terms of additional specification, consider adding – privacy glass, gesture tailgate and the black exterior pack.

On the technical-side, company car and business users can note the P11d at £43,450.00 and CO2 at 151g/km. The 1999CC 8 speed auto diesel engine delivers 47.9 combined MPG (EC), 38.3 (WLTP), 180ps and 0-62 times of 9 seconds. The service intervals on a diesel F-Pace are every 24 months or 21,000 miles.

So would you select the F-Pace as your next leasing option? Or would the Mercedes GLC 4Matic, Audi Q5 Quattro or BMW X3 xDrive be your preferred 4×4 lease car?

Find the best 4×4 lease car deals on the awesome AWD Jaguar F-Pace @CarLease UK – or – check out more 4×4 lease car reviews and deals below…