What is the best SUV (“Coupe”) to lease in 2019? It is quite funny to think that this segment of vehicle was actually non-existent and not particularly popular until about 3 or 4 years ago.

However, as part of the SUV-madness which has swept the UK over the last few years, manufacturers have needed to come up with new solutions both aesthetically and practically to ensure that they meet the needs and requirements of their customer database.

Like the BMW 4 series and Audi A5 Sportback, customers don’t always want the “boxy” style vehicles which traditional saloons and SUVs offered.

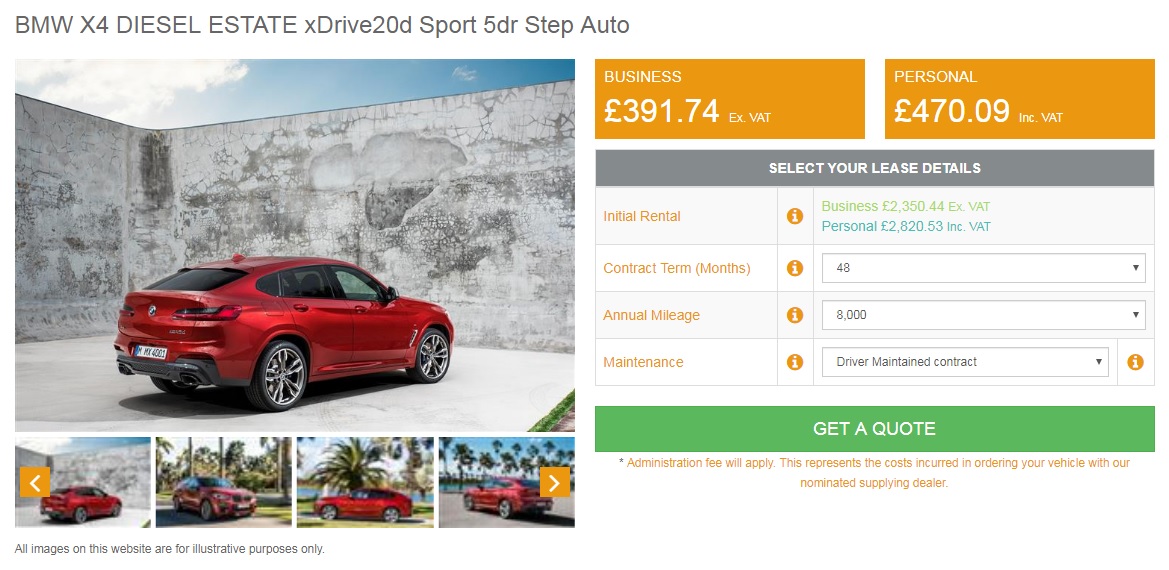

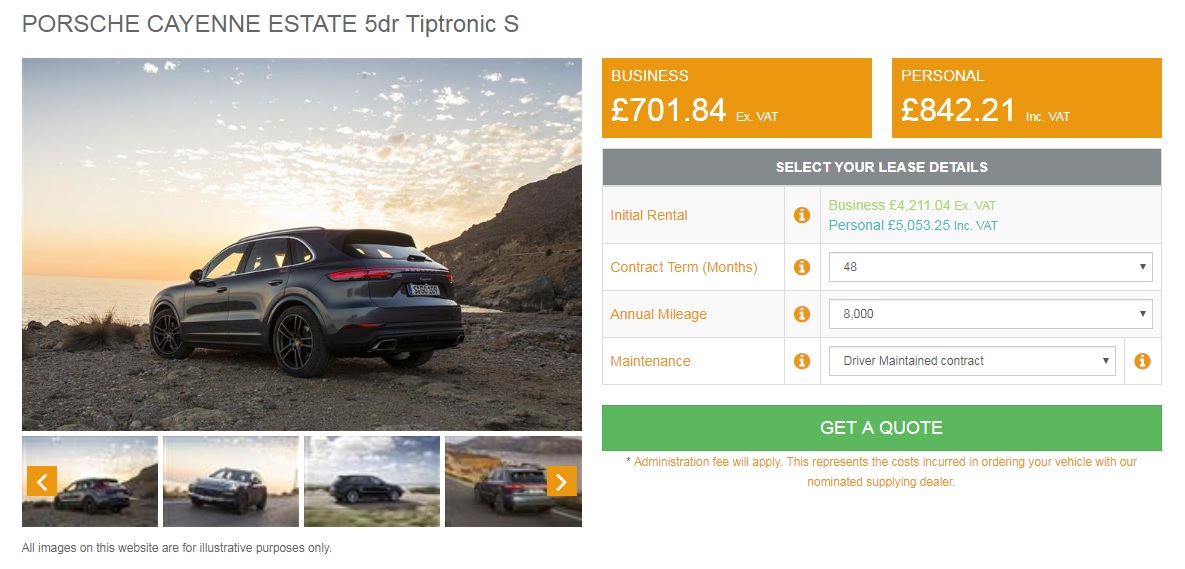

Following suit BMW introduced an X4 (a coupe version of the X3) and the Mercedes GLC Coupe (a sleek version of the SUV model). The high-end luxury car market, the Mercedes GLE coupe, BMW X6 and even the Porsche Cayenne are fulling a new and growing demand.

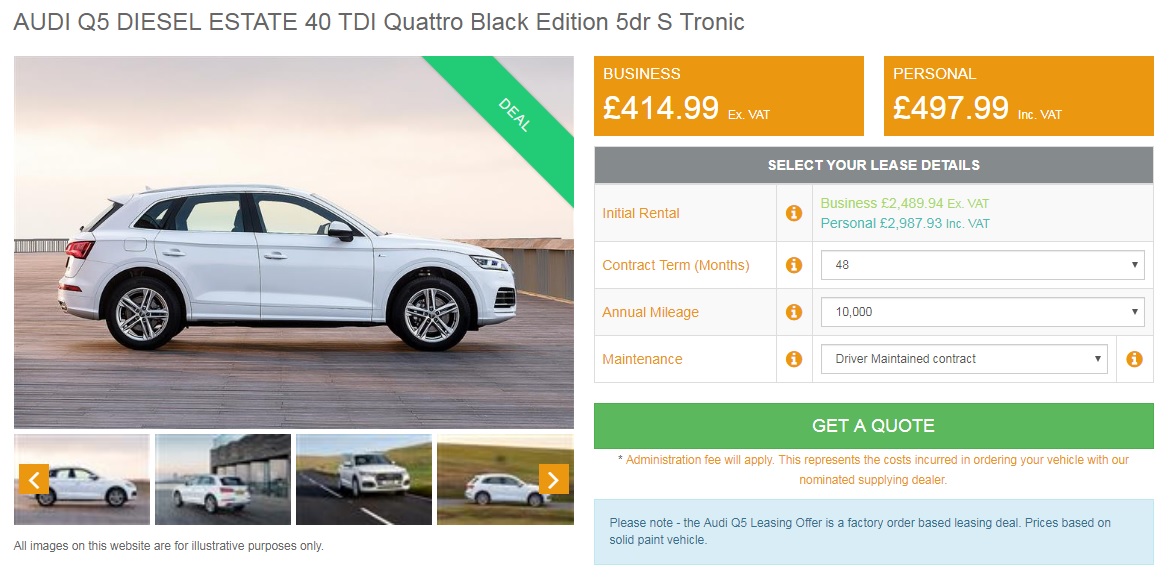

While Audi have only just joined the party with the Audi Q8, there are talks of new smaller product from both them and Jaguar but these will only land with us for pricing circa 2020. In the meantime, the customer is limited to some specific brands, none of which will particularly disappoint you.

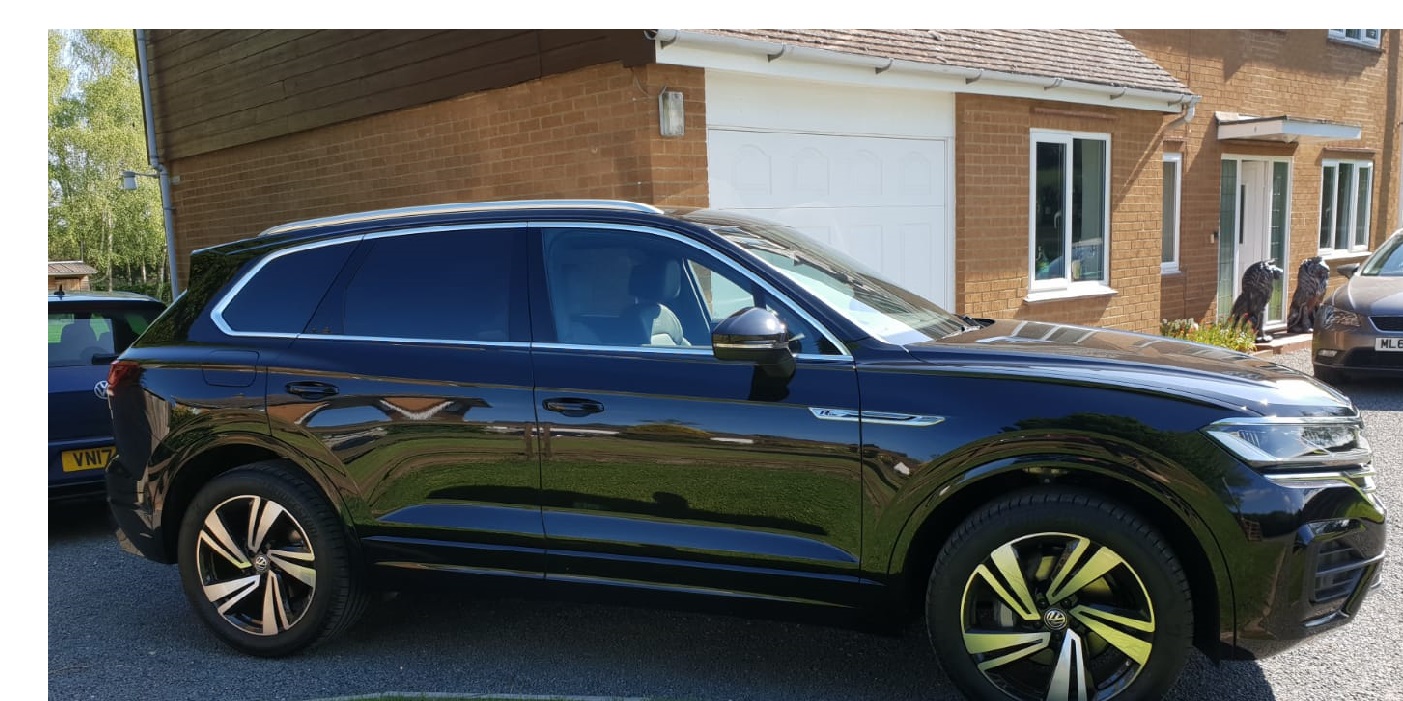

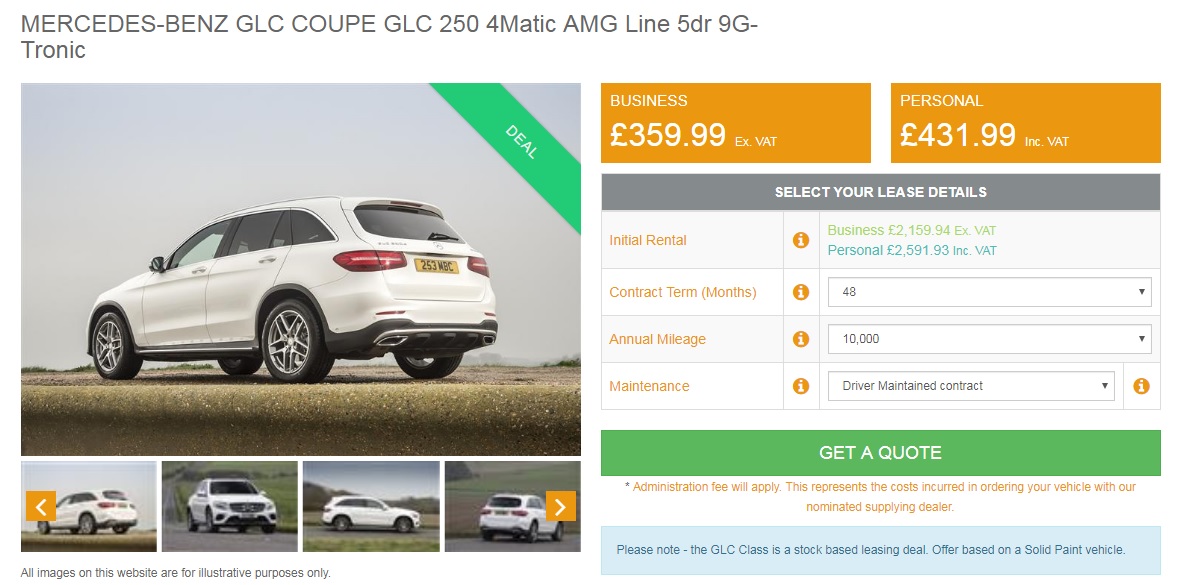

Thank you to our local personal leasing customer, from Wigan (Greater Manchester), for visiting the CarLease UK team to collect their new vehicle – the Mercedes GLC Coupe.

A former company car user, the customer was instead using a personal car allowance to procure a vehicle which was suitable for them.

For some company car drivers there are restrictions under the car policy as to which vehicle they can take whereas those in receipt of a car allowance are often given the full freedom to procure any vehicle which they require.

So if you are receiving a company car allowance, what are the key points to consider?

The first (and often forgotten part) is that a personal contract hire arrangement involves a credit check. J

ust because you are in receipt of a car allowance does not automatically entitle you to receive a car.

When you apply for credit in a leasing agreement, the underwriter will be looking at a) the customer’s willingness to pay; and b) the customer’s ability pay. In terms of the former statement, the underwriter at the finance company (which your credit broker selects) will look at the credit history and consider how you perform with other credit accounts and how (or if) these are settled.

In terms of the latter, this involves a review of your income and expenditure, so is more concerned about the ability meet the demands of the rentals.

For example, with a car allowance situation, if the monthly allowance from the employer clearly meets the costs of the vehicle, its maintenance and insurance, there is strong evidence to suggest that so long as you are employed, this is an affordable proposition. However, if your credit history is such that it raises concerns about your willingness to pay, you may not be accepted for credit. This is why we suggest that for many company car to personal car allowance users credit reference agencies could provide a useful tool.

In addition to the personal responsibility for credit, you also need to be aware that you are taking on the responsibility of the car itself.

When you have a company car, in most situation the company will provide the vehicle, the maintenance (servicing and tyres), breakdown recovery and insurance.

Essentially you get given the keys to the vehicle and you drive it; should anything go wrong the company or the fleet management team will resolve this for you.

However, with a personal car allowance arrangement, you are instead absorbing all of the risk of car usership.

This means that when you get your car allowance you need to, after deducting your income tax from the gross figure, work out the cost of the vehicle, its maintenance/tyres, breakdown recovery and your insurance (plus build a small buffer in for any small issues which could arise). Almost all of the vehicles you see online from credit brokers and finance companies are based on “driver-maintained” arrangements, which presume you will cover the cost of all servicing and tyres. You therefore need to ensure that you ask for a funder-maintained quotation. While the exact terms and conditions of the finance company will differ, in most cases you should get into a position where the amount you pay will cover everything except your fuel and your insurance (although some finance companies are now including insurance on an exceptional basis).

Be careful of pushing your car allowance in order to get a prestige or luxury car, only to find the running cots (whole life costs) are not affordable.

In taking into account all of the above, car allowance customers also need to be clear that leasing is a fixed term usership contract; you never have the right to buy or own the vehicle. In addition, as a fixed term contract this must run for 2, 3 or 4years and there is no ability to simply return the vehicle if your circumstances change.

So am I stuck in a contract hire vehicle? With ANY form of vehicle finance there is often no automatic right to simply hand a vehicle back without a cost consequence. Sometimes, the provision of a voluntary termination under a PCP arrangement make customers mistakenly believe this is possible.

However, for the best part, there are no products which allow this.

If you do wish to return the vehicle, you will need to early terminate the contract, a process which involves paying roughly half of the remaining rentals. For the car allowance customer, weigh up the different terms available and choose one which is likely to practical, rather than one which is simply the cheapest.

In terms of the car shown, the Mercedes-Benz GLC DIESEL COUPE GLC 220d 4Matic Sport Premium 5door 9G-Tronic, this is based on the following configuration:

· Brilliant Blue Metallic Paint

· Artico man-made leather – Black

· Black ash wood trim

· Stainless steel running boards with rubber studs

· 18″ 5 spoke alloy wheels in vanadium silver

As standard the car includes Active park assist with parktronic system, Attention assist, Bluetooth interface for hands free telephone, Collision prevention assist plus, Garmin Map Pilot navigation system with SD card, touchpad and voice control, Instrument cluster with 5.5-inch TFT multi-function display, Mercedes connect me with remote online services, Power opening/closing tailgate, DAB Digital radio, Mercedes Audio 20 radio/single CD + telephone keypad, Adaptive brake lights, Automatic headlights, Black pins diamond radiator grille with integrated stars, Body colour door mirrors and bumpers, Electric sliding glass sunroof, Electrically adjustable and heated door mirrors, LED daytime running lights, LED rear lamps, Privacy glass (to rear of B post), Rain sensor windscreen wipers, 3 spoke leather steering wheel, 4 way adjustable front head restraints, 4 way electric lumbar support, 40/20/40 split folding rear seats, Ambient lighting, Auto Mercedes-Benz child seat recognition sensor, Automatic climate control, Heated front seats, Multifunction steering wheel, Rear top tether child seat ISOFIX attachment, Interior lighting pack – GLC, Memory pack – GLC, Mirror pack – GLC, Storage pack – GLC, Adaptive brake system, Warning triangle and first aid kit, Alarm system/interior protection/immobiliser, Keyless entry and keyless start and 18″ 5 spoke alloy wheels in vanadium silver. In terms of additional options, conside the 360 parking camera or one of the great packs below:

So would you select the GLC Coupe as your next car leasing option?

Find the best lease deals online for the Mercedes GLC Coupe @CarLease UK – or – check out more SUV lease options below.